¿Qué pasa si la autoridad no me localiza para notificar un oficio?

¿Sabías que la autoridad aduanera puede notificarte sin avisar?

En materia Aduanera las notificaciones se realizan generalmente de manera personal por medio de su portal, previo aviso por correo electrónico o medios de comunicación registrados. Cuando la persona que se le quiere notificar un acto administrativo no revisa e ingresa con su e.firma al portal de la autoridad, la autoridad puede emplear la notificación por Estrados.

En muchos casos, el contribuyente no tiene actualizado los medios de contacto ante la autoridad por lo que no recibe los correos de aviso de disposición algún oficio para su notificación, en otros casos el contribuyente sí tiene actualizado los medios de contacto sin embargo puede que los avisos de la autoridad se tengan bloqueados y no se puedan consultar en la bandeja de entrada de los correos electrónicos registrados, o bien, que el contribuyente se le pasen esos correos de avisos y no los atienda.

Cuando se da alguno de estos supuestos y el contribuyente no ingresa a conocer el contenido del oficio que emitió una autoridad, surge el mecanismo de notificación por Estrados, es aquella comunicación que se realiza cuando un acto administrativo, oficio, respuesta etc., dictado por la autoridad no se atiende por el contribuyente, es decir, el Contribuyente no ingresa a la Ventanilla Única para conocer la comunicación de la autoridad.

¿Cuándo se publican las notificaciones en Estrados?

Una vez que la notificación electrónica sea enviada al contribuyente, este cuenta con 5 días hábiles para darse por notificado del acto administrativo que recibió, mediante la firma con su Fiel o e.firma, en términos del Artículo 9º. A y relativos de la Ley Aduanera.

Los 5 días hábiles comenzarán el día siguiente al que fue realizada la notificación del acto, es decir, el día siguiente en el que esté disponible para consultar en su portal es aquel en el que comenzará a transcurrir el plazo.

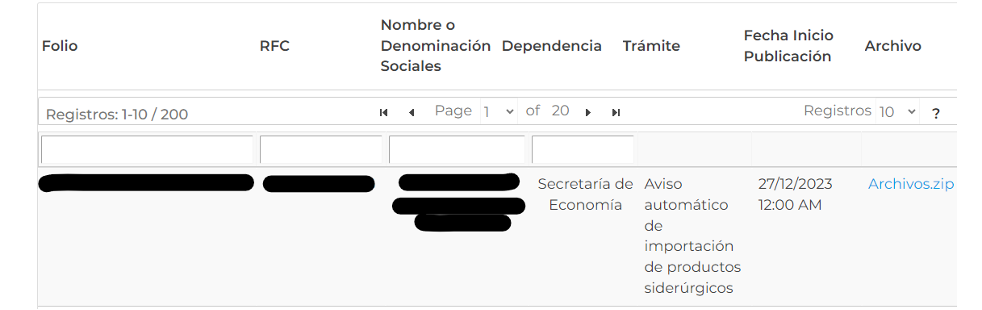

Así pues, transcurridos los 5 días se realizará la publicación en los Estrados que se pueden encontrar en la página oficial de la autoridad que emite; la cual se puede consultar por medio del Folio, RFC, Nombre o Denominación social y por Dependencia que emite. Cuando sea identificado el trámite de su interés puede descargar el oficio en la última columna denominada “Archivo”.

Ejemplo de una notificación por Estrados:

¿Cuándo surte efectos la notificación por Estrados?

Una vez publicado el acto administrativo en los Estrados de la autoridad, se le otorgará al interesado 15 días hábiles para conocer el mismo, al día 16 se dará por notificado el acto, de conformidad con el segundo párrafo del artículo 9º. B de la Ley aduanera.

Fundamento

“…ARTICULO 9o.-B. La notificación por estrados se realizará a través del sistema electrónico aduanero transcurrido el plazo de cinco días hábiles a que se refiere el artículo 9o.-A de esta Ley, para lo cual se publicará el acto administrativo respectivo en la página electrónica del sistema electrónico aduanero por un plazo de quince días hábiles, computado a partir del día hábil siguiente a aquél en que se haya publicado.

Las notificaciones por estrados podrán consultarse en la página electrónica del sistema electrónico aduanero y se tendrá como fecha de notificación el décimo sexto día hábil correspondiente, fecha en la cual surten efectos legales las mismas…”

¿Cómo calcular el plazo de la notificación por Estrados?

Comienza a contarse al día siguiente hábil en el que fue publicado en la página oficial de la autoridad, la cual puede encontrar en la penúltima columna con el nombre “Fecha inicio publicación” o similares.

Cuando se haya identificado la fecha de publicación, se puede determinar el plazo teniendo como día uno el día hábil siguiente de publicación y como último día el décimo sexto hábil, día en el que se considerará como notificado automáticamente el acto. Lo anterior con independencia del plazo que dicte la autoridad en el acto que se notificó.

De igual manera, es importante considerar los días inhábiles que se encuentran en la Ley o Acuerdos que emite la autoridad y publicadas en el Diario Oficial de la Federación (DOF).

“En TLC Asociados desarrollamos un equipo multidisciplinario de expertos en auditorías y análisis de riesgos para asesorar y promover el cumplimiento en operaciones de comercio exterior”.

Para más información o comentarios sobre esta publicación contacte a:

División de Arquitectura y Defensa Legal Aduanera

TLC Asociados S.C.

Prohibida la reproducción parcial o total. Todos los derechos reservados de TLC Asociados, S.C. El contenido del presente artículo no constituye una consulta particular y por lo tanto TLC Asociados, S.C., su equipo y su autor, no asumen responsabilidad alguna de la interpretación o aplicación que el lector o destinatario le pueda dar.

Did you know that the customs authority can notify you without warning?

In Customs matters, notifications are generally made personally through its website, prior notice by e-mail or registered means of communication. When the person who wants to be notified of an administrative act does not review and enter with his/her e.signature to the authority’s portal, the authority may use the notification by Notification List.

In many cases, the taxpayer has not updated the means of contact with the authority so he/she does not receive the notification emails for notification, in other cases the taxpayer does have updated the means of contact, however, the notices from the authority may be blocked and cannot be consulted in the inbox of the registered emails, or the taxpayer may receive the notices and does not respond to them.

When any of these assumptions occurs and the taxpayer does not enter to know the content of the official notice issued by an authority, the mechanism of notification by “Notification List” arises, which is the communication made when an administrative act, official notice, response, etc., issued by the authority is not attended by the taxpayer, that is, the taxpayer does not enter the Single Window to know the communication of the authority.

When are notices published in Notification List?

Once the electronic notification is sent to the taxpayer, he/she has 5 business days to be notified of the administrative act received, by signing with his/her Fiel or e.signature, in terms of Article 9-A and relative of the Customs Law.

The 5 business days will begin the day after the notification of the act was made, that is to say, the next day in which it is available for consultation in its portal is the day in which the term will begin to elapse.

Thus, once the 5 days have elapsed, the publication will be made in the Notification List that can be found in the official page of the issuing authority; which can be consulted by means of the Folio, RFC, Name or Corporate Name and by Issuing Unit. When the process of your interest is identified, you can download the official notice in the last column called “File”.

Example of the Notification List:

When does the notification by Notification List take effect?

Once the administrative act has been published in the authority’s official notice, the interested party will be granted 15 business days to become acquainted with the same, on the 16th day the act will be considered notified, in accordance with the second paragraph of article 9-B of the Customs Law.

Basis

“…ARTICLE 9.-B. Notification by means of a notice through the electronic customs system shall be made after the five working day period referred to in Article 9o.-A of this Law, for which purpose the respective administrative act shall be published on the electronic page of the electronic customs system for a period of fifteen working days, calculated as from the working day following the day on which it is published.

Notifications by means of official notices may be consulted on the electronic page of the electronic customs system and the date of notification shall be deemed to be the sixteenth corresponding business day, the date on which such notifications become legally effective…”

How to calculate the time limit for service by Notification List?

It begins to be counted on the next business day on which it was published on the official page of the authority, which can be found in the penultimate column with the name “Fecha inicio publicación” (Start date of publication) or similar.

When the date of publication has been identified, the term can be determined taking as day one the next business day of publication and as the last day the sixteenth business day, day in which the act will be considered as automatically notified. The above regardless of the term dictated by the authority in the notified act.

Additionally, it is important to consider the non-business days that are found in the Law or Agreements issued by the authority and published in the Official Gazette of the Federation (DOF).

“In TLC Asociados, we develop a multidisciplinary team of experts in audits and risk analysis for consulting and ensuring compliance with foreign trade operations”.

For further information or comments regarding this article, please contact:

Architecture and Customs Legal Defense Division

TLC Asociados S.C.

A total or partial reproduction is completely prohibited. All rights are reserved to TLC Asociados, S.C. The content of this article is not a consultation; therefore, TLC Asociados S.C., its team and its author do not assume any responsibility for the interpretations or implementations the reader may have.